.svg)

Introduction

In the intro to economics section, we discussed what economics was, and the distinction between microeconomics and macroeconomics. Economics is the science of scarcity and studies factors affecting the satisfaction of human wants, and microeconomics studies the individual parts/industries in an economy and the interaction between them.

In this section we will discuss the objectives of microeconomics, and the role that rational choice, opportunity cost and the production possibility frontier ("PPF") play in furthering these objectives.

Microeconomic objectives

The two main objectives of microeconomics are efficiency and equity.

Efficiency

Since resources are scarce, it is important to obtain the most benefit, relative to costs, from available resources. An objective of microeconomics is to increase efficiency in individual parts/industries of an economy and the interaction between them.

Efficiency can be divided into two types:

- Productive efficiency - production is achieved at the minimum possible cost for the maximum possible output; and

- Allocative efficiency - where consumers and producers allocate their resources to achieve the maximum benefit from them, taking into account their preferences i.e. satisfaction of their wants in a way that will bring them the most benefit.

Equity

Even if full efficiency is achieved, some actors in an economy may have more than others. Equity is a value judgement about how resources should be distributed. This judgement will differ depending upon whom you ask, and the ideas of equity in an economy will depend upon its social values.

Microeconomics may model the impact of certain market structures on the distribution of resources, and whether those structures can be changed to achieve a fairer distribution of resources.

Rational choice and opportunity cost

Resources are scarce. Because of this, we often have to make choices between how we use available resources. There are three main categories of microeconomic choice that are made within an economy:

- What goods and services need to be produced, and in what quantities;

- How goods and services are going to be produced; and

- For whom these goods and services are going to be produced.

To increase efficiency when answering the first two of these questions, i.e. increase benefit relative to cost, actors within an economy must make what economists call rational choices; this includes governments, firms and consumers. The third question is to do with equity.

Making a rational choice means weighing up the costs and benefits of an action, and only deciding to do it if the benefits are greater than the costs.

For example, your car needs washing and you have the choice of washing it yourself, or taking it to a car wash. In making a rational choice, you will weigh up the costs and benefits before making a decision. Washing the car yourself may be cheaper, but it might also take longer. You may value doing the manual labour yourself, or you may decide that you prefer doing other things with your time.

Further, choice always involves sacrifice, and a key consideration in making a rational choice is what economists call opportunity cost.

Opportunity cost is the next best thing you could have done with the resources spent in making your choice. Say you decide to take your car to the car wash and it costs £10, and you deem that the next best thing you could have done with that £10 is buy a burrito; the burrito that you did not buy is the opportunity cost of your choice. However, in return you free up the time you would have spent washing the car yourself and you could use this to do other things.

Of course not all actors in an economy make rational choices; firms, consumers and governments may all make bad decisions. There may also be fundamental problems when it comes to making a rational decision; it may be difficult to measure the true cost or benefit of an action, and actors may have imperfect information - meaning they might not know all possible options available to them and may therefore underestimate opportunity cost.

Production Possibility Frontier (PPF)

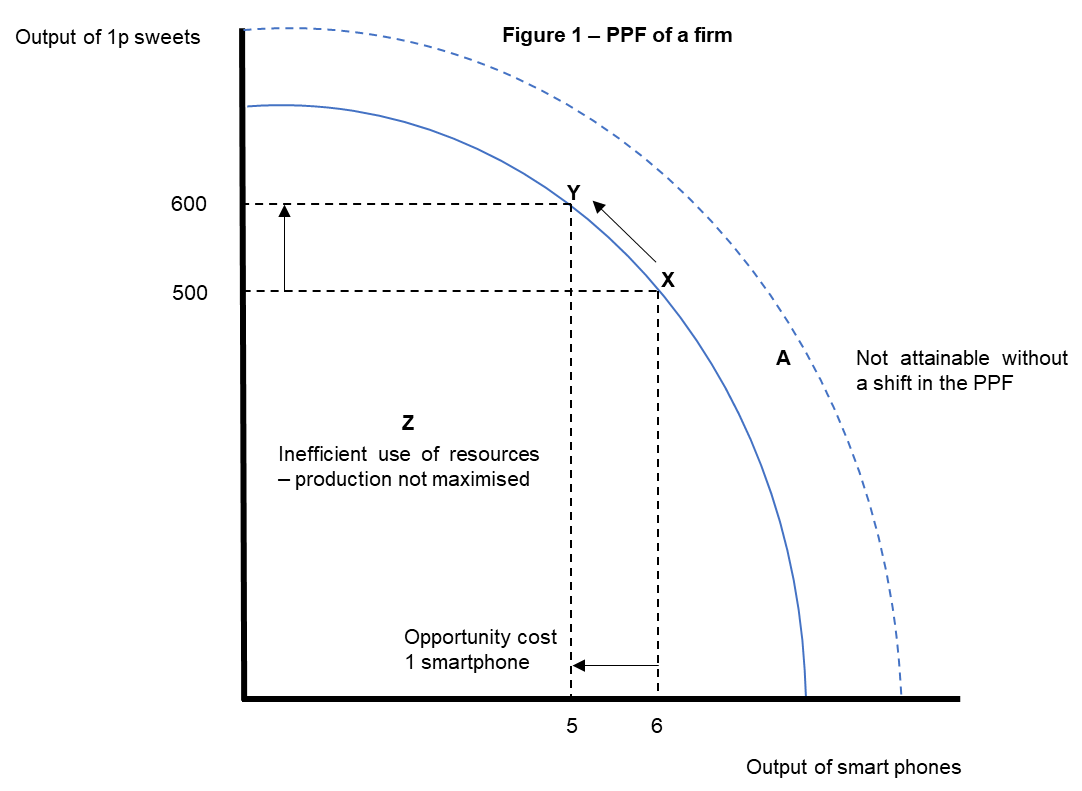

The PPF is an economic diagram exploring the issues of choice and opportunity cost when a country or firm is choosing between which goods or services to produce with its available resources.

When the PPF is modelled for a firm, it is a microeconomic issue. When the PPF is modelled for a country, it is a macroeconomic issue because it deals with the total amount of production in an economy.

Using the diagram below, assume that a country or a firm could only produce smart phones or 1p sweets with its resources.

If a country or firm produces more of one good, it will produce less of the other, giving the curve its downward slope. This illustrates the point of sacrifice and opportunity cost.

For example, a country or a firm is producing at point X, making 500 1p sweets and 6 smart phones, and it decides to move to point Y. The country or firm would then be producing 600 1p sweets but only 5 smart phones (1 less smart phone than at point X). The opportunity cost of the choice is therefore the 1 smart phone that was forgone.

This is a simplification of reality, because it assumes that a country or firm has a choice between producing only two goods or services, when in reality the choice could be between any number. Further, the PPF does not highlight the other factors which could be involved in making a rational choice, such as the value of the goods, the demand for those goods, and the benefit that could be obtained from selling them.

When production occurs on the line of the curve, this assumes that the resources of the country or firm are being used to their fullest. However this isn't always the case in reality, and production may occur inside the curve (point Z on the diagram above), illustrating an inefficient / less than full use of resources.

Point A is outside of the PPF and is not attainable without moving the PPF curve outwards. A firm or country (depending on what the PPF is showing) can push its PPF outwards by increasing the quality and/or quantity of its factors of production - discussed later.

Conclusion

We have now explored the two main objectives of microeconomics – efficiency and equity - and the role that rational choice, opportunity cost and the PPF have in furthering these objectives.

Have a think about how rational choices can improve the allocative and productive efficiency when answering the What and How questions set out above. Also have a look at the actions of businesses in the news and try to think about the costs and benefits (including opportunity cost) they may have considered in making those choices.

.jpg)